Written by Sandeep Singh

| New Delhi |

Updated: November 9, 2017 5:30 am

Appleby documents reveal that GMR Group also executed or sought execution of transactions from the Bermuda law firm that would allegedly help it avoid tax.

Appleby documents reveal that GMR Group also executed or sought execution of transactions from the Bermuda law firm that would allegedly help it avoid tax.

AS PART of its global business expansion plans in infrastructure and energy, the GMR group created a web of companies that involved setting up at least 28 entities across 10 jurisdictions, including Mauritius, the Isle of Man, Spain, Singapore and Malta. These entities were then structured as step-down subsidiaries of GMR Holdings Private Ltd (India).

Appleby documents reveal that GMR Group also executed or sought execution of transactions from the Bermuda law firm that would allegedly help it avoid tax; convert inter-company loans across jurisdictions into compulsory convertible debentures avoid transfer pricing issues; and, in several instances, change the nature of funds (debt to equity and vice-versa) when they were transferred from a subsidiary in one jurisdiction to another.

Also Read | GMR firm bought plane, sold it in two weeks at loss

In 2008, GMR Infrastructure (Malta) Ltd — a subsidiary of GMR Holdings Pvt Ltd (India) — acquired 50 per cent stake in Intergen, a US-based power company through a series of entities and step-down subsidiaries in Mauritius, Cyprus, the Isle of Man, Malta and the Netherlands. The acquisition was routed through GMR Holding (Malta), which took a loan of $837 million of which $637 million was refinanced from Axis Bank Singapore.

However, when the GMR Group decided to prepay a loan of $100 million to Axis Bank in April 2010, it made direct payment to the bank’s Singapore branch from GMR Mauritius, a subsidiary of GMR Holdings India.

The documents include an instruction from a GMR group official to Appleby for passing dummy accounting entries into four companies across three jurisdictions.

Among Appleby data: Email from GMR official seeking change in stake structure.

Among Appleby data: Email from GMR official seeking change in stake structure.

“This prepayment has to be done by April 6, 2010. Considering the number of working days available from now (March 29, 2010) to April 6, it may not be practical to route the US$100mn from Mauritius to Cyprus to Isle of Man to Malta. Hence, we are proposing to make this payment directly from GMR Mauritius to Axis Bank Singapore. However, the entries would be passed in the books of Accounts of Cyprus and Isle of Man companies as though the funds are received from respective parent companies and for Malta this transaction has to be recorded as if the funds were received as CCDs from GMR Energy Global Limited GEGL and repayment of Short Term Loan was made. We would be transferring US$100MM from India to Mauritius by tomorrow. Once the payment is made I will send you the copy of the swift message from Mauritius and you can make appropriate entries in IOM books,” states the instruction contained in Appleby records.

This is one of several instances of innovative accounting and change in nature of funds done by the GMR group in the period between 2009 and 2012 where it was looking to expand its global operations through its presence in Isle of Man.

“GMR Group has a larger emphasis on the business plans for Isle of Companies and these companies would eventually become larger in size in holding investments and centralizing all our business development activities and fund raising initiatives for the group business outside India. Hence, I am of the opinion that the team would gear up to shoulder more responsibilities and be prepared to take up any business proposal with open mind,” a GMR Group official said in a letter to Appleby in January 2010.

Also Read | 714 Indians in Paradise Papers

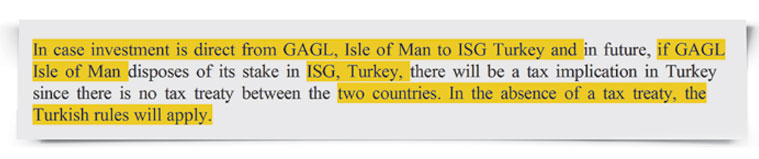

Records show that the Group moved for alleged tax avoidance in other jurisdictions. GMR held 40 per cent stake in ISG International Airport Turkey through GMR Infrastructure Ltd India (35 per cent) and GMR Spain (5 per cent). Records show it decided to move the holding with the Spain entity to a company registered in Malta to benefit from a favourable tax treaty.

“The benefit of investing in ISG, Turkey through MALTA Company will be that Turkey and Malta have favorable tax treaty whereas there is no tax treaty between Isle of Man & Turkey. In case investment is direct from GAGL, Isle of Man to ISG Turkey and in future, if GAGL Isle of Man disposes of its stake in ISG, Turkey, there will be a tax implication in Turkey since there is no tax treaty between the two countries. In the absence of a tax treaty, the Turkish rules will apply,” a GMR official wrote to Appleby.

EXPLAINED: Why the Paradise Papers matter

To achieve this, the Group decided to set up a company in Malta and identified an existing company i.e GMR International (Malta) Ltd, a 100 per cent subsidiary of GMR Infra Mauritius Ltd. The company was later named GMR Airports (Malta) Ltd.

In another instance, looking to repay loans taken by GMR Holdings (Malta), the group instructed Appleby officials to change the nature of funds while transferring it from one group entity to another.

In January 2011, a GMR official wrote to Appleby, stating that while GMR Infrastructure Global Ltd (GIGL, IOM) “will receive $6mn” from its immediate holding company GMR Infra (Cyprus), “the money needs to be treated as share application money and should be transferred to GHML as a contribution to CCD by GEGL which is a step down subsidiary of GIGL (IOM)”.

“These funds are required by Malta to service the interest on the loan taken,” said the GMR official.

SEE PHOTOS | Paradise Papers: Here are the Indians on the list

Experts say financing the operations with debt often results in meaningful reduction of the overall tax rate applicable to the operation. Also, in many jurisdictions, repayment of invested capital (in the form of debt principal) and interest payments is free of withholding tax if the investment qualifies as a debt instrument.

In another instance, GMR Infra SOCIEDAD (GMR Spain) granted an inter company loan to GMR Energy Global Limited, Isle of Man (GEGL), but the money was utilised by GEGL (IoM) among other purposes, for its investment in GMR Malta. While the outstanding inter-company debt was approximately

EUR 27 million and the loan carried an interest rate of Euribor (Euro Interbank Offered Rate, a daily reference rate, published by the European Money Markets Institute).

On this transaction, records show, a GMR official told an Appleby official that GEGL was not in a position to service the interest / repay the loan. The GMR official stated: “Such an outstanding amount along with the fact that the interest rate charged is low will, in the long run, create transfer pricing issues in Spain. Accordingly we are contemplating a restructuring exercise to convert the outstanding loan into CCDs, which will be converted to equity in due course.”

RESPONSE FROM GMR GROUP:

At the outset, we would like to emphasize that GMR group conducts its business in conformity with legislative requirements with transparency to achieve best possible returns to the investors. The entire overseas set-up was done keeping in view various investments in infrastructure projects in overseas the group was planning to undertake, considering the optimum ways to meet the financing needs and to meet the local regulatory requirements. Due care is taken to ensure the resultant investments are well in line with permissible regulations both domestically and in overseas.

Also Read | Secrecy of tax havens smashed, says Jaitley, orders action; all to be probed, says tax chief

GMR Group iswas having business entities in various jurisdictions like Turkey, Singapore, Indonesia, Nepal, Philippines, etc. The business of infrastructure where separate business entities need to be set up for each project/activity on account of concession agreements, multiple partners necessarily need large number of companies. The entity in Mauritius is the first level subsidiary through which all overseas investments are done by listed entity. In view of specific needs to cater to the investment in Intergen BV, we had to set up Isle of Man and Malta entities which are in the process of closure post Intergen divestment. Currently, we do not have any entity in Spain. The Singapore entity is involved in the construction of airport terminal along with our partner in Philippines. All these entities are set up in line with extant regulations governing investments, tax treaties, and full disclosures are made to respective authorities on the activities of these entities regularly.

The investment in Intergen NV was made through an entity in Malta as Intergen is set up as a company in that jurisdiction and because of the Netherlands preference for investments from Europe over other countries, we had to necessarily do the investment in that way. The investment was done through step-down subsidiaries taking into account our existing overseas subsidiary at Mauritius through which we have to make all overseas investments as per RBI regulations, the existing tax treaty agreements between Mauritius and ultimate country of investment, ie., Netherlands and the future plans of listing of this entity in overseas exchanges for which Isle of Man was preferred in between.

As you may be aware, Intergen NV is a well-diversified utility company registered in Netherlands having generation facilities in Netherlands, UK, Mexico, Philippines, Australia totaling 8,000 MW with another 4,600MW in development. We acquired 50% stake in this company and other shareholder was Ontario Teachers Pension Plan Board. As mentioned, the entire investment was made in line with the above structure.

As regards payment to Axis Bank, the same was done by GMR entity in Mauritius directly as the entity in Mauritius was the ultimate overseas holding company in charge of the investment and considering the need to close the loan on due date to facilitate completion of investment transaction. There is nothing unusual in the transaction and such direct remittances do happen many a time to save on the time and costs involved. As long as all the entities involved accept the completion of transactions, there is no irregularity or violation of any law. The direct payment was resorted to as the loan to Axis Bank was to be paid on 6th April, 2010 as per notice already served and sending the funds through all the companies involved would have delayed the remittance as each transfer would have taken one business working day considering USD remittance and we would have missed the payment due date.

It is not correct to say GMR group has transferred ISG investment to a group company in Malta to evade taxes in foreign jurisdiction. The re-organisation of shareholding was done to rationalize the overseas chain of companies post our Intergen divestment. As we understand, Turkey and Malta do not enjoy a favourable tax treaty compared to Turkey and Spain and ultimately Malta Revenue Authorities have confirmed our tax status in year 2014.

There are occasions on which the nature of funds transferred from one entity to another entity is changed subsequent to transfer of funds. These were primarily cases of miscommunication or on account of changes proposed in the capital structure which are in line with local jurisdictional laws.

Restructuring of investments do happen because of change in business requirements like fresh investments, divestments which warrant reclassification of investments in subsidiaries. Also, we may have to reclassify investments based on local laws which need to be complied with like Income Tax and Corporate Laws governing debt and equity. The Group has followed all relevant laws and regulations in conducting its business including investments.

GMR Group is/was having operations in various countries and at times making investments from different companies in various jurisdictions becomes necessary considering the availability of funds at that particular point of time and time involved in transferring money from one country to another country. There is no complexity in these transactions and required documentation for each of these transactions was done before completion of remittances. It is common for directors in charge of individual companies to raise certain questions before taking up a transaction and sufficient support is always provided for. In view of investments in different jurisdictions and different partners, we need to necessarily maintain different holding companies to facilitate encumbrances by various financing banks and at times the jurisdiction of holding company do depend on banks’ compliance requirements also.

Click here for full coverage on Paradise Papers

For all the latest India News, download Indian Express App

Go to Source

Appleby records show that JP Morgan wanted the documents prepared for the share transactions vetted within three days.

Appleby records show that JP Morgan wanted the documents prepared for the share transactions vetted within three days.